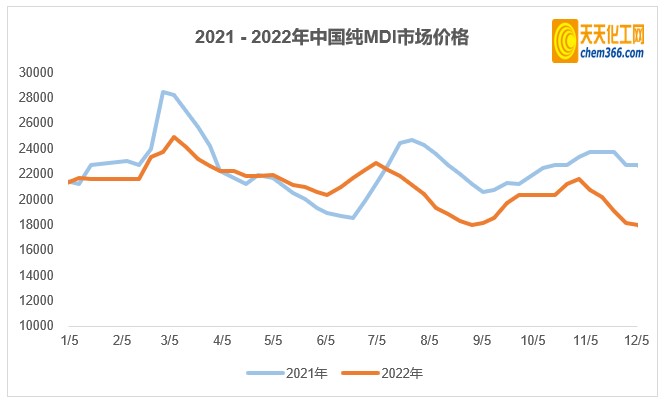

December, the domestic pure MDI market continued to decline, and the recent trend has a wide range of corrections.

As of the afternoon of December 5, the quotations of domestic mainstream agents were around 16,500 yuan/ton, which was a drop of 800-1,000 yuan/ton within a week compared with 17,000-17,500 yuan/ton at the end of November. The current market price is at the lowest price since the beginning of 2021, and the market presents a weak bottoming pattern.

(The lowest price in 2021 is 18,400-18,800 yuan/ton in June, and the lowest price in January-October 2022 is 17,800-18,300 yuan/ton).

Supplier:

In November, the Yantai unit was overhauled, and the rectification units in Shanghai and Chongqing were reduced successively. Therefore, the overall operating rate of domestic MDI distillation units dropped significantly in that month, and the output shrank. In addition, mainstream manufacturers lowered their listing prices in December month-on-month, following the trend of the market. However, the follow-up performance of downstream demand has continued to be poor recently, and manufacturers are still under pressure on shipments. On the distribution side, agents also maintain active shipments, negotiate with profit sharing to promote transactions, while the overall inquiries and buying momentum in the downstream are weak, and the volume of transactions is lacking.

Demand side:

In November, the downstream demand of pure MDI was “slower in the off-season”. The main reason is that the terminal consumption of textiles, shoes and clothing is not good, which leads to the decline or low operation of pure MDI downstream factories. Spandex industry: In November, the overall start-up rate of spandex was about 70%, and the supply of manufacturers was relatively sufficient. However, most downstream weaving factories mainly consumed the previous inventory, and the intention to purchase raw materials was weak. Therefore, the price of spandex was weak and fell by about 10% that month. Slurry and sole solution industry: In November, the slurry and sole solution industry was affected by the epidemic and the downturn in terminal consumption, and the “off-season was even weaker”. The overall operation starts at a low level (40% to 50% of the stock solution for soles; about 30% for the slurry industry).

December Market Outlook

Supply side: In December, manufacturers are expected to start operations steadily, and sales of pure MDI will still be dominated by shipments. As the price fell below the low level of the year, it is expected that the market will increase cautiously.

Demand side:

The accumulation of textile industry has increased, and the holiday time has been brought forward

This year’s textile market has left many weaving factories in deep trouble. As early as the beginning of November, some companies in the market revealed plans to have a holiday soon. Recently, the order volume of weaving companies is not as good as in previous years, and the production enthusiasm of factories is not high, showing a downward trend. The number of factories on holiday in December has gradually increased, which means that this year’s market is basically over. Although there will be opportunities to replenish orders and reorders in the “Double Twelve” later, the extremely high return rate of e-commerce has caused new fatigue in clothing inventory. library. According to a stretch fabric company, the overall order volume during the “Double Eleven” period this year is not as good as in previous years, and the “Christmas season” orders have also “shrunk” a lot. If there is no new order added, you may choose to take a holiday in advance. On the one hand, you can effectively control labor costs, and on the other hand, you can arrange payment collection earlier.

The epidemic pushes up the inventory of terminal textile enterprises

For the downstream textile industry, the main terminal of pure MDI, in the first half of 2022, the domestic textile business experienced a domestic epidemic, the industry was shut down, and the vitality was seriously injured. At present, although it is already recovering, textile enterprises still face the pressure of clearing a large amount of inventory. And near the end of the year, the financial gap of the enterprise is increasing, and “removing cash from the warehouse” has become the top priority of the current enterprise, and the demand for its own recent production plan and procurement of production raw materials is relatively weak.

Based on the above-mentioned industry difficulties, Fujian Province, as the center of the textile industry, has issued special loans to help enterprises bail out in recent months. According to the news on December 4, the Fujian Provincial Department of Finance disclosed that Fujian Province took the lead in setting up a special loan for the textile, footwear and apparel industry with a scale of 5 billion yuan on October 14. A number of textile and footwear enterprises. It is understood that the total revenue benefiting enterprises this time accounts for about 1/5 of the province’s textile, footwear and apparel industry, covering upstream and downstream enterprises in the industrial chain such as chemical fiber, cotton spinning, weaving, dyeing and finishing, shoes and apparel, as well as textile, footwear and apparel machinery, industrial Internet, etc. Supporting industries such as platforms.

Downstream end of pure MDI: In summary, it is expected that the overall downstream demand for pure MDI in China will improve somewhat in December. Waiting for the recovery and boost of terminal consumption after the optimization of the epidemic prevention policy, and the progress of reducing the pressure on terminal enterprises.